Syria Needs More Electricity. Does It Matter Who Builds It?

Why ownership matters less than procurement, regulation, and the cost of supply

Executive Summary

Syria’s electricity sector is entering a new phase in which private investors may participate in the construction and operation of power plants. This development has sparked public concern that the introduction of private generation could lead to higher electricity prices or allow private firms to exercise excessive market power.

This policy paper argues that private participation in electricity generation does not inherently lead to higher prices. On the contrary, if new plants operate more efficiently than existing facilities, their introduction can reduce the overall cost of electricity generation and improve supply reliability. Such benefits, however, depend on the strength of the regulatory and procurement framework. Transparent dispatch rules, well-designed power purchase agreements, and effective oversight are essential to ensure that private participation helps expand electricity supply without increasing costs.

As such, the central policy question for Syria is not whether electricity generation should be public or private, but whether the institutional framework governing the sector ensures that all generators, whether public or private, operate efficiently and in the public interest.

Syria’s Electricity Crisis and the Need for Investment

Syria’s electricity sector has experienced a severe deterioration in generation capacity since 2011, driven by infrastructure damage, fuel shortages, aging power plants, and limited maintenance. Over more than a decade of conflict, large portions of the country’s power infrastructure were damaged or destroyed. Current generation capacity went from 9,838 MW in 2011 to 5,403 MW in 2023. This loss in generation capacity is broken down into about 1,771 MW (18% of 2011 capacity) being totally destroyed, and many other plants requiring major repair.1 Still, fuel constraints have reduced the country’s available generation capacity to around 1,800 MW in 2024, less than one-fifth (18%) of the capacity in 2011.

As a result, national electricity generation has declined dramatically. Total electricity production fell from approximately 49,260 gigawatt-hours (GWh) in 20112 to around 16,454 GWh in 2024 (-67%).3 At the same time, technical losses in the network increased, going from about 26% in 2011 to 33% today. These losses reflect both physical damage to the transmission and distribution system and operational challenges, including maintenance deficits and electricity theft.

This state of play has left Syrians with only a few hours of electricity per day, pushing households and businesses to resort to alternative coping mechanisms, generally involving expensive off-grid solutions, such as privately operated diesel generators. These generators supply electricity through neighborhood micro-grids at extremely high prices, sometimes reaching ten times the estimated grid supply cost.

The relevant consumer comparison is therefore not only between state-owned and privately financed grid generation. In much of Syria, households and businesses already rely on private diesel generators, solar systems, batteries, and other off-grid solutions. These are often far more expensive than formal grid electricity. If private investment helps restore a reliable grid supply and displaces informal diesel generation, households may experience lower effective electricity costs even if official grid tariffs rise from their historically subsidized levels.

Recognizing electricity as a cornerstone of economic recovery, Syria’s interim authorities have prioritized the rehabilitation of the power sector, combining short-term fuel supply arrangements with longer-term infrastructure investment.

In the short term, authorities have sought to increase generation by securing natural gas imports from regional partners, including Qatar and Türkiye. Qatar had agreed to supply gas through Jordan to fuel the Deir Ali power plant, potentially generating about 400 MW of additional electricity, while Türkiye had arranged deliveries of roughly 6 million cubic meters of gas per day, enough to generate around 1,200 MW in Syrian power plants. These fuel imports were intended to temporarily raise generation and extend daily electricity supply, although they remain insufficient to restore pre-war output given the destruction of infrastructure and the limited operational capacity of many plants.

At the same time, the government is attempting to address the structural supply gap through large-scale investment projects. The most prominent initiative is a USD 7 billion memorandum of understanding signed in May 2025 with an international consortium led by Qatar’s UCC Holding, alongside Türkiye’s Kalyon Enerji and Cengiz Enerji, and supported by U.S.-based Power International Holding (PIH). The agreement initially outlined the construction of four combined-cycle gas turbine (CCGT) power plants with a total capacity of around 4,000 MW, together with a 1,000 MW solar project. In November 2025, the Syrian Ministry of Energy and the consortium signed the final concession agreements, allowing the projects to move toward implementation. The contracts provide for the construction of four large natural-gas-fired combined-cycle plants located in North Aleppo (1,200 MW), Deir Ez-Zor (1,000 MW), Zeyzoun (1,000 MW), and Mhardeh (800 MW), as well as four solar projects totaling 1,000 MW distributed across several regions.

It should be noted, however, that the contractual structure and pricing arrangements of these projects remain unclear. This has led to speculation about the future of the country’s electricity sector, with the emergence of private investment sparking public debate.

Even if new private plants produce electricity cheaply, their effect on consumer supply will remain limited unless transmission and distribution bottlenecks are addressed. Syria’s electricity crisis is therefore not only a generation crisis, but it is also a grid crisis. Damaged transmission lines, substations, distribution losses, theft, and limited system control can prevent low-cost generation from reaching consumers. In that context, generation investment and grid rehabilitation must be treated as complementary, not interchangeable.

Historically, Syria’s electricity system has been organized around vertically integrated public entities responsible for generation, transmission, and distribution. Electricity dispatch is coordinated centrally through the national control center, while the Public Establishment for Transmission and Distribution of Electricity (PETDE) acts as the system operator and effectively functions as a single buyer procuring electricity from generators and supplying it to distribution networks and major consumers, as per Legislative Decree No. 9 of 2020.

In such a system, concerns about generator pricing power are limited when generation assets are entirely state-owned. However, as privately owned power plants enter the system, questions may arise about how electricity will be priced and how potential market power will be regulated. It should be noted that although private participation in electricity generation is now becoming politically and commercially more significant, the legal opening is not entirely new. Law No. 32 of 2010 already allowed domestic and foreign private investment in generation and distribution. What is new is the scale, urgency, and strategic importance of private generation in the post-2024 recovery context.

Understanding whether these concerns are economically justified requires examining how electricity costs are actually determined within power systems. In practice, the cost of supplying electricity is primarily driven by generation costs and dispatch decisions, rather than by whether generation assets are publicly or privately owned. In systems where electricity is procured through centralized dispatch or long-term Power Purchase Agreements (PPAs), the relevant comparison is between the cost of electricity supplied by different power plants within the generation fleet. This distinction is central to assessing the potential impact of new private investments in Syria’s electricity sector.

Understanding Electricity Pricing: Marginal Cost and the Merit Order

Even in centrally dispatched electricity systems such as Syria’s, system operators typically schedule power plants according to their operating costs. In practice, plants with lower operating costs are dispatched first, while higher-cost plants are brought online only when demand exceeds the capacity of cheaper generators.

This operational logic is commonly referred to as the merit order. Under the merit order, generators are ranked from lowest to highest marginal cost of production, meaning the cost of producing one additional unit of electricity. As electricity demand rises, the system operator progressively dispatches plants along this cost curve until total supply meets demand.

In Syria’s electricity sector, new private generators are likely to sell electricity to the state through long-term PPAs with the PETDE. Under such arrangements, the state commits to purchasing electricity at a predetermined tariff, typically expressed in USD/MWh.4 The economic impact of such contracts depends largely on how the PPA tariff compares to the marginal cost of existing power plants in the national generation fleet.

To illustrate this principle, consider three hypothetical power plants that generate the same amount of electricity with marginal production costs of $40, $60, and $80 per MWh. If electricity demand is high enough that all three plants must operate, the system operator must dispatch the most expensive plant in order to meet demand. In that case, the state’s average electricity generation cost would be $60/MWh. During periods of lower demand, however, the system may only require the two cheaper plants. In that situation, the average cost of electricity generation falls to $50/MWh, since the $80 plant is no longer needed.

The fiscal implications are straightforward. If electricity tariffs are set below the actual cost of production, the government absorbs the difference through subsidies. The more expensive the plants that must be dispatched to meet demand, the higher the average cost of electricity generation and, therefore, the greater the fiscal burden on the state. Conversely, if electricity tariffs reflect production costs, as seems to be the current government’s aim, a lower generation cost will translate into lower electricity bills for consumers.

Now consider adding a new, more efficient power plant that can produce electricity at $20/MWh under a long-term Power Purchase Agreement (PPA) with the state. Because this plant produces electricity at a lower cost than the existing generators, it would be dispatched first. As a result, more expensive plants would be pushed further down the merit order, and the $80/MWh plant might no longer be required to operate during periods of high demand. In that case, electricity would be generated by the $20, $40, and $60 plants, bringing the average electricity generation cost down to $40/MWh. By reducing the need to run the most expensive generators, the new plant would lower the overall cost of electricity supply and reduce the government’s fiscal burden and consumers’ electricity bills.

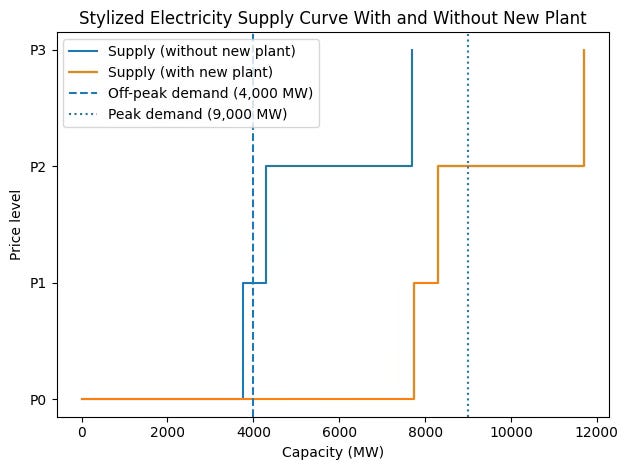

Illustrative electricity supply and demand curves. The addition of large-scale, efficient generation shifts the supply curve outward, lowering generation costs at a given level of demand. In this example, at a demand level of 4,000 MW, the introduction of a new power plant reduces the market price from P1 to P0. At a demand level of 7,000 MW, the price would also fall significantly, as power plants producing at price levels P1 and P2 would no longer need to be dispatched.

Of course, the magnitude of these savings ultimately depends on the terms of the PPA and the efficiency of the new plant, which determine whether the contracted tariff is actually lower than the cost of existing generation.

Building a more efficient plant should not be difficult in Syria, as the country’s generation fleet is largely composed of aging thermal power plants with widely varying efficiency levels. Indeed, older steam units and simple-cycle gas turbines, which account for a large share of Syria’s installed thermal capacity (see table above), consume significantly more fuel per unit of electricity than modern CCGT plants, the technology planned for the new facilities to be developed by the consortium.

Risks and Opportunities: Market Power and Regulatory Oversight

In the context of electricity sector reform, there may be concerns about private generators, given the possibility that a dominant firm could abuse its market position to raise electricity prices.

Indeed, electricity systems are often considered vulnerable to market power: firms can influence prices because demand is relatively inelastic in the short term, supply must match demand at all times, and generation capacity may be limited during peak periods. In fully liberalized electricity markets, these characteristics can allow generators to influence prices by withholding capacity or strategically bidding above their marginal costs.

However, Syria’s electricity system is unlikely to operate as a competitive wholesale electricity market in the near term. Instead, electricity from privately financed plants will most likely be procured by the state through long-term PPAs within a centralized single-buyer system.

In such systems, the primary risk is not real-time price manipulation but rather the possibility that electricity procurement contracts are poorly structured or negotiated at excessively high tariffs. If governments sign PPAs with prices that exceed the cost of existing or alternative generation options, the overall cost of electricity supply might not be as low as it could be, even if the private plants themselves operate efficiently.

These risks can take several forms:

capacity payments: Many PPAs include payments for availability or capacity, not only for the electricity actually generated. The state may therefore pay even when the plant is not fully dispatched.

take-or-pay obligations: The public buyer may be required to pay for a minimum quantity of electricity or plant availability regardless of actual system demand.

currency risk: If the PPA is denominated in USD while consumers pay in Syrian pounds, the government carries exchange-rate risk.

sovereign guarantees: Investors may require state guarantees if PETDE or the relevant public utility is not considered sufficiently creditworthy.

For this reason, the key policy challenge is to maintain a robust regulatory and procurement framework governing the sector. Governments typically rely on several mechanisms to ensure that private participation remains aligned with the public interest:

transparent procurement processes, such as competitive tenders, which allow governments to benchmark electricity prices and select the most cost-effective projects;

contractual performance obligations, including availability requirements and penalties for unjustified outages;

regulatory oversight and monitoring, allowing authorities to review generator performance and ensure compliance with contractual obligations.

well-designed PPAs, which define tariff formulas, payment structures, and operational responsibilities.

Under such conditions, private participation is most likely to lead to an expansion of generation capacity without necessarily increasing electricity supply costs.

In the Syrian context, new privately financed power plants could reduce electricity generation costs, particularly if they introduce, as promised, newer, more efficient technologies than those currently operating in the public generation fleet. Still, the economics of new gas-fired generation will depend heavily on fuel availability and pricing. Modern CCGT plants can reduce generation costs only if they have reliable access to gas at predictable prices. If gas must be imported, financed externally, or purchased in foreign currency, the apparent efficiency gains of new plants may be partly offset by fuel-price and exchange-rate exposure.

Today, much of Syria’s existing thermal generation capacity consists of aging power plants built between the late 1970s and early 2000s. Many of these facilities suffer from outdated turbine technology, low thermal efficiency, high fuel consumption per unit of electricity generated, and significant maintenance constraints after years of conflict and limited investment. As a result, the marginal cost of producing electricity at several existing plants is relatively high.

By contrast, modern CCGT plants generate electricity more efficiently by using both gas and steam turbines to extract additional energy from the same fuel input. This significantly reduces fuel consumption per unit of electricity produced, lowering generation costs. If new projects introduce such technologies under reasonably priced PPAs, they are likely to be dispatched before older, less efficient plants, thereby reducing the overall cost of electricity supply.

However, this outcome is not automatic. The potential cost benefits of private generation depend heavily on how investment projects are structured, negotiated, and procured. If electricity purchase agreements are signed at tariffs that exceed the marginal cost of alternative generation options, the introduction of private plants could increase the overall cost of electricity supply even if the plants themselves are technically efficient.

This risk is particularly relevant in contexts of institutional transition and urgent reconstruction needs. When governments face severe electricity shortages and strong pressure to rapidly expand generation capacity, large energy agreements may sometimes be negotiated quickly and with limited competitive procurement or regulatory scrutiny. In such circumstances, the absence of transparent tenders or benchmarking against comparable projects can make it difficult to ensure that electricity tariffs reflect the lowest achievable cost.

For this reason, the economic impact of private generation ultimately depends on the quality of procurement processes, contract design, and regulatory oversight, rather than the ownership structure of power plants. Transparent bidding procedures, cost benchmarking, and robust institutional review mechanisms are essential to ensure that private investment contributes to expanding electricity supply while keeping generation costs as low as possible.

Policy Implications for Syria

The debate over private participation in electricity generation should focus less on ownership and more on the institutional framework governing procurement, contracts, and system oversight. Private investment can help expand generation capacity and introduce more efficient technologies, but the economic outcome depends heavily on how projects are selected, negotiated, and regulated.

For this reason, strengthening governance and transparency in electricity procurement should be a central priority of Syria’s reconstruction strategy. Key priorities include:

Competitive and Transparent Procurement: Electricity generation projects should be awarded through transparent and competitive processes, such as international tenders. The Ministry of Energy has already issued dozens of tenders open to international bidders, mostly to procure energy resources, while tenders for infrastructure projects have been extremely limited. Competitive bidding via infrastructure-related tenders allows governments to benchmark electricity tariffs against comparable projects and select proposals offering the lowest cost of supply, reducing the risk of overpriced contracts. Going forward, encouraging multiple independent power producers and diversifying generation sources can prevent excessive reliance on individual suppliers, strengthen the government’s bargaining position in future procurement processes, and contribute to a more resilient and cost-efficient electricity system over time.

Careful Structuring of PPAs: PPAs should include clear tariff formulas, transparent indexation mechanisms for fuel costs and inflation, and well-defined performance obligations. Properly structured contracts can ensure that electricity tariffs reflect the actual cost of generation while protecting the public sector from excessive long-term financial commitments. Such contracts are frequent, and the Syrian government, especially the Directorate for Contracts and Loans at the PEEG, should refer to international best practices supported by international organizations.

International Technical Support and Benchmarking: Syria may benefit from technical assistance from international financial institutions such as the World Bank, the International Monetary Fund, and regional development banks to design procurement frameworks, benchmark electricity tariffs, and review major infrastructure contracts. Such cooperation can help ensure that new generation projects follow international best practices and remain financially sustainable.

Strengthening Regulatory and Institutional Oversight: A technically capable, independent regulatory framework is essential for supervising generator performance and monitoring contract compliance. Establishing or strengthening an independent electricity regulatory authority, or encouraging external audits, could play an important role in enhancing transparency and investor confidence. In that regard, support should be provided to the PEEG and PETDE in the lead-up to the implementation of large-scale private generation projects.

Parliamentary and Public Oversight of Major Energy Contracts: Given the long-term fiscal implications of large electricity projects, major PPAs and energy infrastructure agreements should be subject to appropriate parliamentary review, scrutiny, and oversight. Greater transparency in contract approval processes can strengthen public accountability and help build confidence that electricity investments serve the national interest.

Conclusion

The entry of private investors into Syria’s electricity generation sector does not inherently imply higher electricity prices. Electricity supply costs are determined primarily by generation efficiency and dispatch decisions, rather than by whether power plants are publicly or privately owned. As such, if new private plants operate at lower marginal costs than existing state-owned facilities, their introduction can reduce overall system costs while improving the reliability of electricity supply.

The key determinant of outcomes will be the strength of regulatory oversight. Transparent dispatch rules, effective cost monitoring, and well-structured contractual frameworks are essential to ensure that private participation helps expand electricity supply without increasing costs. Ultimately, the central policy challenge lies in establishing governance mechanisms capable of ensuring that all generators—public or private—operate in the public interest, not in the presence of private investors.

According to the World Bank, the Aleppo Thermal Station (2015), Zeyzoun in Idlib (2016), and Thayyem in Deir Ez-Zor (2017) were destroyed during the conflict, while other major facilities, including the Mhardeh, Al-Zara, and Tishreen thermal power plants, sustained significant damage and require extensive repairs.

According to data from the Planning and Statistics Authority, formerly known as the Central Bureau of Statistics.

According to data from the Public Establishment for Electricity Generation (see Table 1).