Syria Monthly Economic Digest - May 2026

External re-engagement, energy and transit ambitions, financial reform, and the domestic pressures testing Syria’s recovery.

Welcome to the May 2026 edition of the Syria Monthly Economic Digest. Each month, I select the political and economic developments I think matter most for Syria’s transition, summarise what happened, and explain why it matters.

This is not meant to be an exhaustive news roundup. The aim is to track the developments that reveal where the country is heading — from reconstruction and investment to banking, energy, public services, property rights, and the evolving relationship between the state and society.

This month’s digest covers nine developments across four broad themes: Syria’s external re-engagement with Europe and the Gulf; energy, electricity, and regional connectivity; financial and banking reform; and the domestic social tensions emerging around wheat procurement, makeshift oil refineries, and Decree 66-linked reconstruction projects.

You can read more about The Syria Dispatch and the purpose of this publication at the end of the post. If you have comments, corrections, or suggestions, you can also find my contact details there and reach out directly.

Syria’s External Re-Entry: Diplomacy, Gulf Capital, and Strategic Positioning

Business Delegation Signals UAE Investment Push as Alabbar Floats Multi-Billion-Dollar Projects

Key Developments: Syria–UAE economic engagement accelerated in May with the first Syrian–Emirati Investment Forum in Damascus and a high-level UAE business delegation led by UAE Minister of Foreign Trade Thani al-Zeyoudi. The delegation met President Ahmad al-Sharaa and included more than 120 Emirati companies and institutions. The visit coincided with renewed Emirati interest in Syria following an earlier visit by Emaar Properties founder Mohamed Alabbar, who said he was assessing investments worth up to USD 18 billion, including USD 5–7 billion on the Syrian coast and up to USD 11 billion in Damascus and its surroundings. It was also reported that Alabbar-linked Eagle Hills is studying two much larger master-planned projects in Dummar and Latakia, with a combined development cost exceeding USD 50 billion, though the projects remain in the early stages of discussion.

While Syrian officials used the forum to promote investment incentives and regulatory reforms, some Emirati investors raised concerns over exchange-rate stability, banking and transfer mechanisms, sovereign guarantees, and the need for clearer regulatory frameworks. Despite the scale of the projects discussed, no signed investment agreements or memoranda of understanding were publicly announced, although it was reported that the two sides had reached preliminary agreements on several investment tracks.

UAE Foreign Trade Minister Al-Zeyoudi said bilateral non-oil trade reached USD 1.4 billion in 2025, up more than 130% year-on-year, while discussions focused on industry, agriculture, renewable energy, logistics, the digital economy, tourism, aviation, and private-sector partnerships. Separately, the UAE announced support for the restoration of the Umayyad Mosque in Damascus, adding a cultural dimension to renewed bilateral engagement.

Why It Matters: The Syria–UAE forum marks a genuine Emirati rapprochement, but one likely to remain cautious, transactional, and step-by-step. Abu Dhabi moved more slowly than Qatar and Saudi Arabia after Assad’s fall, partly because of its long-standing hostility to Islamist movements, its unease with HTS’s links to Türkiye and Qatar, and its previous rapprochement with the Assad regime. The UAE is therefore not simply “returning” to Syria; it is testing the new authorities through trade, investment, heritage diplomacy, and high-level business channels. Sharaa’s visit to Abu Dhabi earlier in April and his public solidarity with the UAE helped accelerate this opening, while the UAE officials also publicly noted Syria’s support. Still, the relationship carries a trust deficit on both sides.

The visit also needs to be read through the lens of Gulf competition. Both Qatar and Saudi Arabia are much better positioned in Syria, and the UAE does not want the post-Assad transition to become an arena shaped only by these players, including Turkiye. Abu Dhabi wants a stake in the emerging economic order, especially in real estate, ports, logistics, aviation, tourism, digital services, and urban development. But the large figures attached to Alabbar and Eagle Hills should be treated as positioning rather than implementation, especially given the difficulties most prospective investors face in moving from signing to implementation of their investments.

The Israel angle is also important, though it should not be reduced to a formal precondition for normalization. The UAE may continue to engage Syria without waiting for a Syria–Israel agreement, but Abu Dhabi could also serve as an additional channel for indirect contact between the two sides. It was previously reported that the UAE had facilitated secret indirect talks between Syria and Israel. From an investment perspective, it is difficult to imagine large-scale Emirati capital flowing into Syria while the risk of Israeli escalation remains high, or while Israel may view Emirati investment as strengthening a state it still treats as an adversary. A formal Syria–Israel normalization deal may not be required, but some form of security understanding, de-escalation mechanism, or tacit Israeli acceptance would likely be more conducive to UAE–Syria rapprochement and investment.

EU–Syria Dialogue Marks Shift from Isolation to Structured Re-Engagement

Key Developments: On May 11, Syria and the EU held their first High-Level Political Dialogue in Brussels, co-chaired by Syrian Foreign Minister Asaad al-Shaibani and EU High Representative Kaja Kallas. The meeting focused on EU–Syria relations, regional stability, Syria’s inclusive political transition, socio-economic recovery, and reconstruction. It took place alongside the Syria Partnership Coordination Forum, co-chaired by al-Shaibani and EU Commissioner for the Mediterranean Dubravka Šuica, with EU Member States, G7 countries, Arab states, the UN, and major financial institutions in attendance.

The EU announced work on a EUR 15 million Technical Assistance Hub to support Syrian institutions, a EUR 14 million contribution to rehabilitate Al-Rastan Hospital in Homs, and preparations for the additional EUR 280 million in socio-economic support for 2026–2027. The dialogue also coincided with a major legal step: the EU Council restored the full application of the 1977 EU–Syria Cooperation Agreement, ending the partial suspension imposed in 2011 and reopening the agreement’s trade and economic-cooperation framework.

The month also showed that Syria’s re-engagement with Europe is expanding beyond Brussels. Syrian President Ahmad Al-Sharaa had joined a European Council summit with regional partners in Cyprus in late April, where discussions focused on the Middle East, the EU’s southern neighborhood, and regional security. Sources say he used the meeting to present plans for Syria to become a regional transit and energy corridor, an argument Damascus is expected to repeat in upcoming G7 discussions, which Syria will attend as a guest nation.

At the same time, the EU maintained its conditional approach. Syrian activists and MEPs urged Brussels to link deeper engagement to human rights, accountability, minority protection, and an inclusive transition. On May 25, the EU Delegation to Syria also published its updated Roadmap for Engagement with Civil Society, stressing the need for adaptive and sustained support to Syrian civil society, which it described as central to community resilience, advocacy, dialogue, and participation. Separately, the EU renewed targeted sanctions against individuals and entities linked to the former Assad regime until June 1, 2027, while delisting seven entities, including the Ministries of Defense and Interior.

Why It Matters: The High-Level Political Dialogue confirms that EU policy toward Syria is moving from containment to structured re-engagement, but not to unconditional normalization. Restoring the Cooperation Agreement and launching formal political dialogue reopen channels that had largely collapsed after 2011. Yet the renewal of targeted sanctions and the publication of the civil society roadmap show that Brussels still wants engagement to remain tied to inclusion, accountability, and institutional reform.

For Damascus, the stakes are practical. Europe offers technical assistance, reconstruction financing, trade normalization, regulatory support, and political legitimacy. Syria is also trying to reposition itself not only as a recovery file, but as a strategic connector between the Gulf, Iraq, Turkey, the Mediterranean, and Europe. The transit-hub argument is useful because it gives European governments a reason to see Syria as part of their energy, logistics, and supply-chain calculations, not only as a source of refugees or instability. But it remains more a strategic pitch than a delivered reality: pipelines, ports, borders, electricity links, customs systems, security guarantees, and financing all still need to be made functional.

For the EU, Syria is now tied to migration management, refugee returns, counterterrorism, regional stability, energy security, and influence in the Eastern Mediterranean. This gives Damascus leverage, but also puts it under assessment. The coming test is whether both sides can move from political signaling to operational cooperation: credible institutions on the Syrian side, usable instruments on the EU side, and enough delivery on services, infrastructure, civil society participation, and economic governance to make re-engagement visible beyond diplomatic meetings.

Energy and Connectivity: From Resource Recovery to Transit Ambitions

Offshore Exploration Deals and Iraqi Oil Transit Seek to Revive Syria’s Energy Sector

Key Developments: On May 11, Syria identified an offshore block for its first deep-water oil and gas exploration project with Chevron and Qatar’s UCC Holding, paving the way for final contracts and technical operations to begin in the summer. One day later, the Syrian Petroleum Company signed a memorandum of understanding with ConocoPhillips, TotalEnergies, and QatarEnergy to conduct technical studies, prepare a work program, and draft an exploration contract for offshore oil and gas exploration in Block 3 near Latakia. Separately, INA Croatia and MOL Group (Hungary) held talks with Syrian counterparts over a possible restart of projects suspended since 2012.

Onshore, the Syrian Petroleum Company continued efforts to restore production in eastern Syria. In Deir Ezzor, SPC restarted wells 110 and 116 at the al-Tanak field, adding around 800 barrels per day to the current output. The company said al-Tanak had produced 50,000–60,000 barrels per day before 2011, but that 90–95% of its infrastructure had been damaged, leaving current production at around 3,000–5,000 barrels per day. Still, amid constrained oil supplies, it was reported that Russia had become Syria’s dominant crude supplier after Assad’s fall, with shipments rising by 75% to around 60,000 barrels per day in 2026.

Iraqi oil also became an increasingly important part of Syria’s energy and transit picture. Iraq sent its first crude shipment to Syria through the reopened Rabia–al-Yarubiyah crossing in early May, with an initial 70 tanker trucks, while the Syrian Petroleum Company raised daily unloading capacity for Iraqi oil at Baniyas refinery to around 500 tankers, up from 300. Iraq’s Oil Ministry also discussed opening an Iraqi shipping office at Baniyas port and reviving the Iraqi–Syrian oil pipeline, while Baghdad separately announced plans for a 700-kilometre Basra–Haditha pipeline with a planned capacity of 2.5 million barrels per day and possible export routes toward Baniyas, Ceyhan, and Aqaba. At the same time, SPC said recent increases in domestic petroleum-product prices were driven by higher supply, transport, production, storage, maintenance, insurance, and global fuel costs, and were intended to maintain stable distribution across governorates.

Why it Matters: The return of the main eastern oil fields to government control is economically significant, but it should not be mistaken for a rapid return to pre-war production. Syria’s oil output had already been declining long before 2011, after peaking in the 1980s, and the war then accelerated the collapse through infrastructure destruction, sanctions, underinvestment, primitive refining, smuggling, and repeated changes in control. This does not mean recovery is impossible. New drilling, reservoir management, digital monitoring, enhanced oil recovery, horizontal wells, and better seismic interpretation could make some previously marginal fields or old discoveries more viable today than they were 15 years ago.

But Syria is not, and has never been, a major oil power capable of living off hydrocarbons without major discoveries. Even at its historic peak, its output was modest by regional standards, and much of the known onshore base is mature, damaged, or under-assessed. But that is why offshore exploration, albeit speculative, still matters: it offers upside that the mature eastern fields may not. It should be noted, however, that Syria has not yet made a commercial offshore discovery, and Lebanon’s nearby offshore campaigns have so far failed to produce a positive discovery.

This makes the more ambitious targets floated by SPC leadership. SPC Director Youssef Qiblawi said current output had reached around 133,000 bpd, projected roughly 300,000–350,000 bpd by end-2027, and repeated a target of around 800,000 bpd by late 2029 or early 2030. His explanation relied on a combination of rehabilitating damaged fields such as al-Omar and al-Tanak, expanding Rmeilan, and drilling new onshore blocks. While these targets are politically important because they signal confidence to investors and the public, they remain highly ambitious given the state of infrastructure, reservoir damage, financing needs, and operational risks.

Nevertheless, offshore exploration is technically complex, and that is precisely why it matters. A single exploration or delineation well can cost close to USD 100 million before any production is guaranteed, so any move toward drilling involves mobilizing substantial capital, personnel, and technical capacity in Syria. For now, however, the sector’s near-term significance lies in credibility, capital inflows, and energy security. Agreements involving Chevron, TotalEnergies, ConocoPhillips, QatarEnergy, and UCC can bring technical studies, seismic work, drilling commitments, service contracts, and foreign capital even before production begins. Onshore investment will remain more constrained and will depend, among other things, on investors’ ability to price political, legal, insurance, and operational risks and move capital into Syria.

Electricity Supply Improves Unevenly as Syria Moves to Restore Regional Power Links

Key Developments: Syria’s electricity sector continues to see localized improvements, although supply remains uneven across regions. In Aleppo, electricity returned gradually to parts of the eastern city after around nine years of interruption, following the opening of four transformer centers in al-Shaar, benefiting roughly 15,000 residents. The Ministry of Energy also said it had carried out transmission, distribution, and maintenance works across several regions, including restoring electricity to Hurran in rural Maarat al-Numan after 13 years, raising supply in 286 villages around Qamishli from one hour to more than eight hours per day, and bringing electricity back to 35% of Qamishli city after a two-year outage. Separately, the Jandar power plant in Homs reportedly reached full production capacity for the first time in nearly a decade, rising from around 200 MW before the transition to 825 MW after maintenance works.

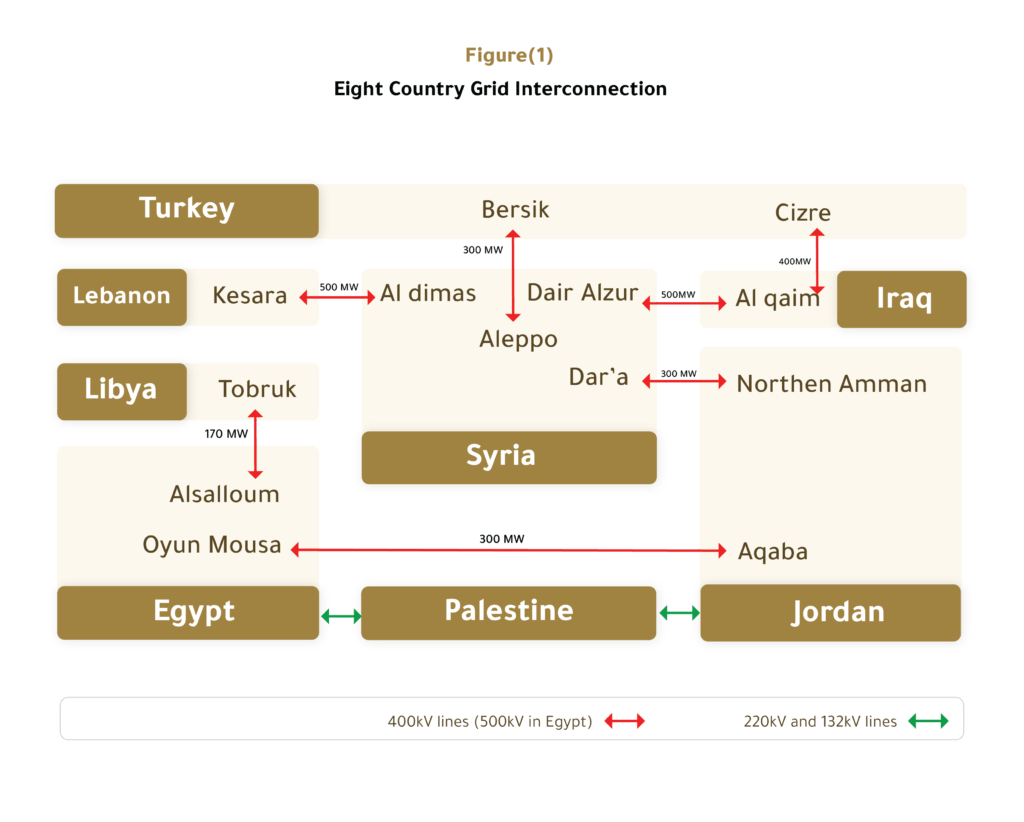

Regional electricity interconnection also returned to the policy agenda. In Amman, the Syrian, Jordanian, and Lebanese energy ministers discussed advancing electricity interconnection and related technical work, with Syrian Energy Minister Mohammad al-Bashir saying Syria was working to rehabilitate power links with Jordan and Lebanon. Syria plans to restore transmission lines with Jordan and maintain four interconnection lines with Lebanon, which officials described as technically ready on both sides. Furthermore, Lebanon’s energy minister later said Beirut was considering buying electricity directly from Syria, while work continues on the wider Jordan–Syria–Lebanon interconnection, which he said could take around one year to rehabilitate.

Despite these improvements, electricity remained a source of pressure for households and industry. In Aleppo, industrialists reported electricity bills reaching millions of Syrian pounds after industrial tariffs rose to SYP 1,700 per kWh (+/- USD 0.13) for factories requiring continuous supply, while some industrial areas still received only around 12 hours of power per day. Separately, legal challenges against the October 2025 tariff increase continued in Syrian courts, with hearings delayed into June. In Idlib, local sources also reported new tariff increases by the Turkish private company Green Energy, alongside recurring evening outages.

Why It Matters: The Syria–Jordan–Lebanon electricity track reopens an old regional interconnection file that had long been technically plausible but politically difficult. Jordan and Syria have been linked through a 400 kV transmission line since 2001, but suspended in 2012. The 2022 plan to transmit Jordanian electricity to Lebanon via Syria stalled over financing, infrastructure damage, and sanctions-related complications. With Syria now re-engaging diplomatically, sanctions barriers reduced, and Lebanon still facing severe power shortages, using Syria as an electricity corridor has become more practical again.

Domestically, supply is improving from a very low base. Better electricity in Damascus, Aleppo, Qamishli, Raqqa, Deir Ezzor, and other areas matters because power remains one of the main constraints on recovery. A more reliable supply reduces dependence on private generators, lowers operating uncertainty, and allows households, workshops, and factories to operate for longer hours. Politically, restoring electricity to long-neglected areas and places only recently brought under central government control also helps the state reassert itself through service delivery, especially in eastern and northeastern regions where authority and infrastructure were fragmented during the war.

The risk is that improved availability is being paired with higher tariffs before reliability is fully restored. The recent tariff reform may help reduce subsidy pressures and improve sector finances, but it also raises production costs for manufacturers, food processors, textile producers, metal workshops, and other energy-intensive activities. If firms pass these costs on, consumers face higher prices; if they cannot, margins narrow and production remains constrained, with the labor market also potentially being affected.

Financial Normalization: Central Bank, Currency, and Public Banks

Central Bank Unveils New Strategy as Raslan Replaces Husrieh

Key Developments: On May 15, President Ahmad al-Sharaa appointed Mohammed Safwat Raslan as Governor of the Central Bank of Syria, replacing Abdulkader Husrieh, who was subsequently appointed Syria’s ambassador to Canada. Shortly before his departure, Husrieh had announced the Central Bank’s 2026–2030 strategy, which focuses on monetary stability, exchange-rate management, banking-sector integrity, digital payments, financial inclusion, and reintegration into the global financial system.

The Central Bank also formally launched a sector-wide gap assessment with consultancy firm Oliver Wyman covering both the Central Bank and the wider financial sector. Separately, reports indicated preparations for a Damascus Foreign Exchange and Gold Market intended to provide a centralized platform for foreign-exchange trading and price formation.

High on the Central Bank’s agenda, currency replacement remained a central policy priority throughout the month. On May 1, the Central Bank extended the exchange period for old banknotes until June 30, while Husrieh reported that 56% of the old monetary mass had already been replaced. By the end of May, Raslan extended the deadline again until July 30 and announced that replacement rates had exceeded 63% nationwide. Throughout the month, the Syrian pound traded at roughly SYP 13,500–14,000 per USD ((new) SYP 135-140) in the parallel market, remaining significantly weaker than the official exchange rate.

Why It Matters: The replacement of Abdulkader Husrieh with Safwat Raslan came at a sensitive moment for Syria’s monetary transition. Husrieh had overseen several key post-Assad initiatives, including the currency replacement process, the 2026–2030 strategy, and the Oliver Wyman gap assessment, and was at the forefront of efforts to reconnect Syria’s financial system with international institutions. Husrieh’s sudden reassignment, therefore, sends mixed signals, especially given the lack of public criticism against him: it may reflect an effort to bring in a younger, more implementation-oriented figure with experience in private banking, governance, and digital transformation, but it also raises questions about policy continuity and the degree of autonomy granted to the Central Bank, especially given reports of competing influence within the institution itself.

At the policy level, the new strategy broadly targets Syria’s main financial weaknesses: low confidence in the pound, a fragmented foreign-exchange market, weak banking intermediation, limited digital payments, and the need to reconnect with global financial channels. As for the currency replacement process, it shows progress, but the repeated extensions and the recent decision to reopen exchanges through exchange and transfer companies also suggest that the Central Bank is still adapting the rollout to administrative bottlenecks, weak banking coverage, and the realities of a cash-based economy. Reopening the process to exchange and transfer companies matters because bank-branch coverage remains uneven, especially outside major cities, while money-transfer networks have long been central to Syrian cash circulation.

Public Banks Enter Reform Push as Debt Relief, Lending, and Governance Issues Advance

Key Developments: Syria’s public banking sector saw several reform-related developments in May. Oliver Wyman reportedly completed the first phase of its review of Syria’s six state-owned banks, with options under discussion including restructuring, privatization, or strategic partnerships. Separately, Finance Minister Mohammad Yisr Barnieh met with directors of public banks to discuss the implementation of Presidential Decree No. 70 of 2026 on distressed loans, while the Ministry of Finance later issued executive instructions covering exemptions, rescheduling, and settlement mechanisms for borrowers at government banks.

Several public banks also announced operational measures. The Agricultural Cooperative Bank prepared its branch network to pay farmers’ grain dues during the wheat season, and issued instructions for settling farmers’ distressed loans under Presidential Decree No. 70 of 2026. The Popular Credit Bank resumed limited-income loans with a ceiling of (new) SYP 100,000 (+/- USD 720), though debate later emerged over loan interest rates following an earlier Court of Cassation ruling on usurious interest. The Industrial Bank and the Ministry of Finance also discussed launching a Sharia-compliant banking window and financing tools to support the repair of damaged industrial facilities.

Governance and integrity concerns remained visible. Oversight reporting raised allegations of embezzlement linked to Saving Bank offices. Separately, the Ministry of Finance announced disciplinary and anti-corruption measures against 256 employees and accountants, adding that future lists would include employees in government banks.

Why It Matters: Public-sector banks were cornerstones of Syria’s development in previous decades because they served as the primary financial channels through which Syria allocated credit to specific social and productive groups. The Agricultural Cooperative Bank is designed to finance rural communities and agricultural activities; the Industrial Bank to support industrial projects; the Popular Credit Bank to serve low-income borrowers and small productive activities; and the Real Estate Bank to finance housing and construction.

This makes the reform debate politically sensitive. The Oliver Wyman review, therefore, raises a central policy question: should Syria modernize its public banks, privatize them, or preserve them as development-oriented institutions? Given the government’s broader shift toward a more liberal economic agenda, including discussions around the privatization of state-owned enterprises, which has yet to be settled, such a move would not be surprising. Yet a reform agenda focused mainly on profitability could weaken the banks’ development role, especially if institutions originally designed to serve farmers, industrialists, small borrowers, and housing finance are pushed toward purely commercial lending.

The resumption of lending is one of the most important signals in the public banking sector because formal credit had virtually disappeared during the conflict. In 2020, Syrian authorities ordered public and private banks to stop granting credit facilities, including at the Real Estate and Agricultural banks, and Syria’s broader banking collapse severely weakened access to credit for businesses and households. Against that backdrop, Presidential Decree No. 70 of 2026 and the reopening of Popular Credit Bank lending could prove significant. Presidential Decree No. 70 of 2026 is designed to clean up non-performing loans through interest waivers, penalty exemptions, and rescheduling, while the Popular Credit Bank’s return to personal lending gives limited-income public-sector employees access to formal credit again.

The Islamic finance debate adds another layer. Syria already has an Islamic finance base: Islamic banks greatly outperformed traditional banks throughout the conflict, with rising demand for Islamic tools such as murabaha and Islamic bank assets growing from SYP 18.2 trillion to SYP 25 trillion. The government is also exploring sukuk: Finance Minister Mohammad Yisr Barnieh said Syria was working on the legal, regulatory, and technical framework for the country’s first sovereign sukuk issuance, while debate has emerged over whether such instruments should finance productive projects or simply cover budget gaps. The debate over the use of sovereign sukuk issuance is not new, as the Ministry of Finance was reportedly already finalizing a draft regulation to legislate such financial instruments in 2024.

Taken together with the Popular Credit Bank’s return to interest-based lending, the proposal to allow Islamic banking windows, and the renewed public debate over bank interest, these developments raise broader questions about the government’s financial direction. The issue is not Islamic finance itself, which can broaden participation and attract savers or borrowers who avoid conventional interest-based products, and which has proved to be extremely popular. The risk is that debates over “usurious interest” could narrow the space for ordinary credit precisely when Syria needs multiple financing channels. There is also a question of sequencing. Given the state’s limited legislative and administrative bandwidth, prioritizing new Islamic-finance frameworks while existing financial tools remain underused could slow more urgent reforms.

Finally, this debate also intersects with uncertainty about the government’s willingness to take on loans. Observers continue to ask whether the reluctance reflects a preference for interest-free or Sharia-compliant financing, concerns over already mounting public debt, or simply the difficulty of accessing affordable external credit. It remains to be seen whether will be whether Syria builds a plural financial system (conventional, Islamic, development-oriented, and donor-backed) or whether ideological and fiscal constraints limit the range of tools available for broad-based economic recovery and reconstruction.

The Domestic Social Contract: Wheat, Property, and Livelihoods

Wheat Price Protests Force Bonus as Stronger Harvest Season Tests Grain Procurement

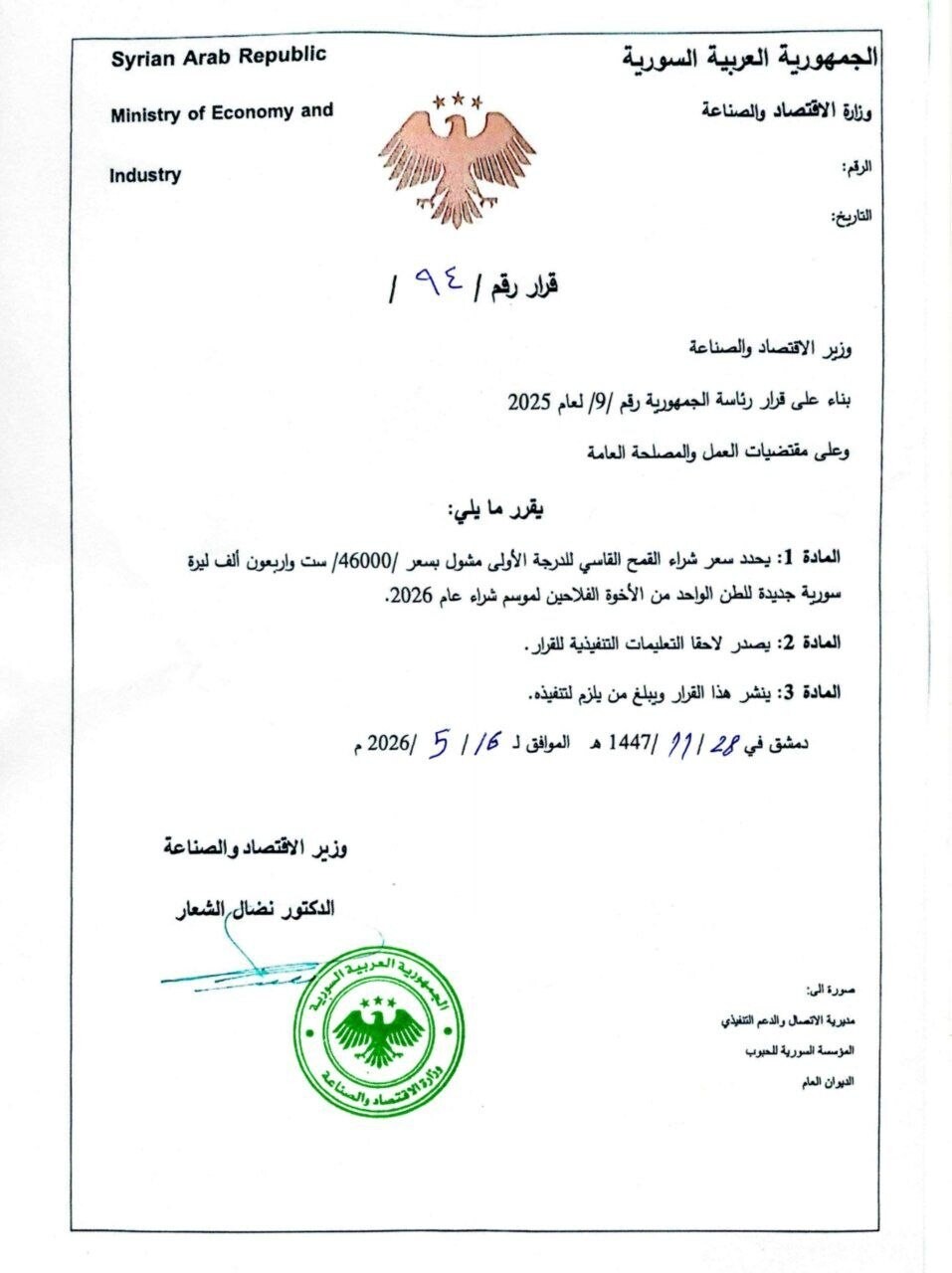

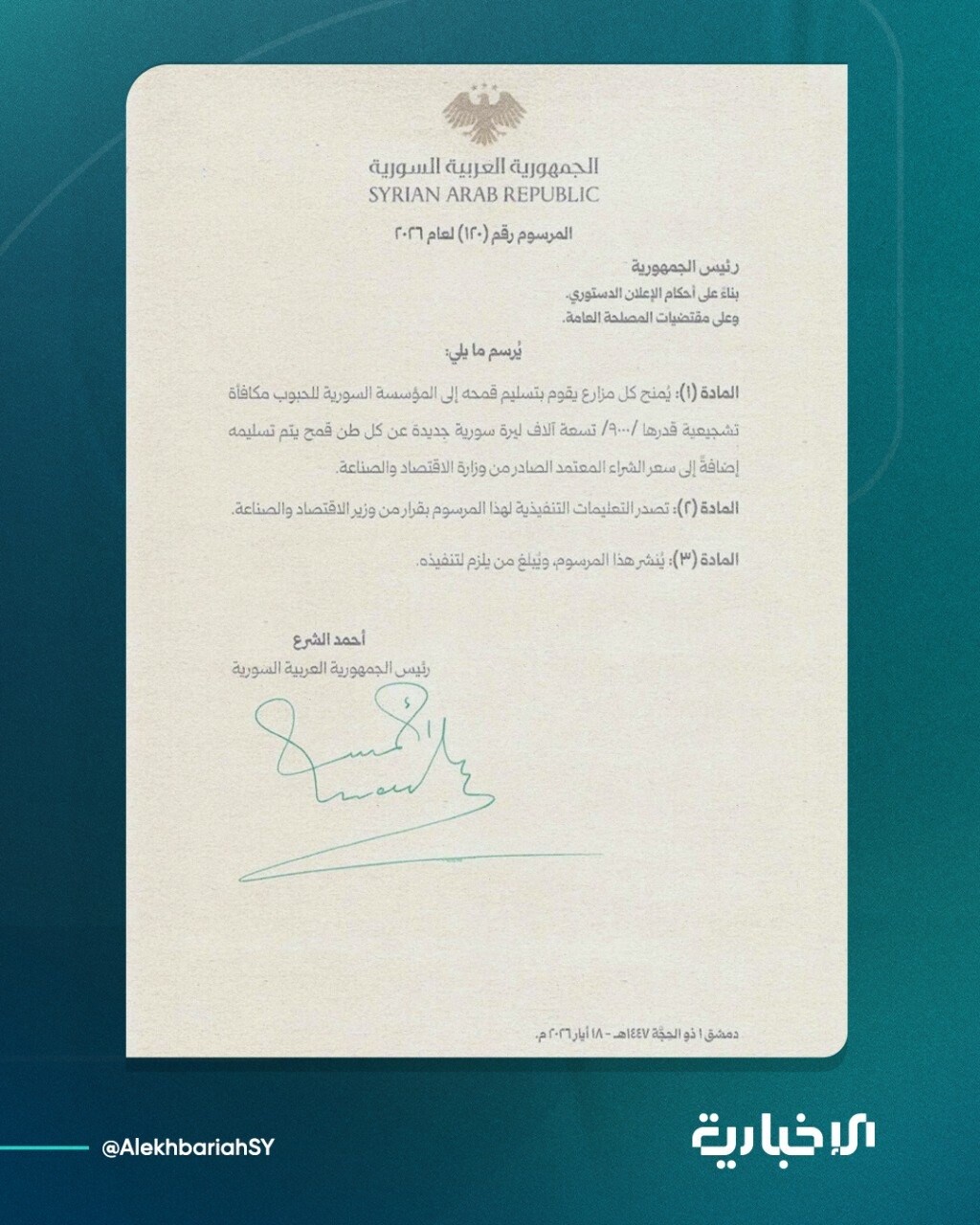

Key Developments: Syria’s 2026 wheat season became a major policy issue after the Ministry of Economy and Industry set the purchase price for first-grade durum wheat at (new) SYP 46,000 per ton (+/- USD 333), triggering farmer protests in several wheat-producing areas. Farmers and residents protested in Raqqa, Deir Ezzor, Hasakah, Hama, and other agricultural areas, arguing that the price did not reflect higher costs for fuel, seeds, fertilizers, harvesting, transport, and sacks. Al-Modon also reported that some farmers threatened to withhold deliveries to state institutions if the price was not revised. In reaction, President Ahmad al-Sharaa issued, on May 21, Presidential Decree No. 120 of 2026, granting wheat farmers an additional (new) SYP 9,000 per ton (+/- USD 65) delivered to the Syrian Grain Establishment, on top of the official purchase price. This raised the effective state purchase price to (new) SYP 55,000 per ton.

{kind=link}

{kind=link}

The government also moved to prepare procurement and payment channels for the harvest. The Syrian Grain Establishment said it had raised storage capacity to around 1 million tons, was preparing 15 new sites in Hasakah, Raqqa, and Deir Ezzor, and planned to expand its marketing and intake centers to nearly 80. The Agricultural Cooperative Bank separately said that 106 branches were being prepared to pay farmers’ grain dues, except for 24 branches in Hasakah and Raqqa, where payments would be redirected to nearby operational branches.

The season unfolded against a mixed agricultural backdrop. Heavy rainfall improved vegetation and water availability after a significant drought during the preceding season, but also caused flooding, damage to farmland, and disruption to infrastructure in several areas.

Why It Matters: Syria relies on a state-led foodgrains procurement model in which the government buys wheat from farmers through official grain institutions to secure flour supplies, bread availability, and strategic reserves. The stakes were especially high after two weak seasons and a severe drought. The FAO had forecast Syria’s wheat import requirement for the 2025/26 marketing year at around 3 million tonnes, nearly 70 percent above the five-year average, while it was previously reported that domestic production had fallen far below national consumption needs in 2025.

These protests are noteworthy for their scale, their status as a nationwide mobilizing issue, and for showing that farmers potentially represent a significant bargaining force in the post-Assad transition. The initial price increases triggered demonstrations in half of Syria’s governorates, with some farmers threatening to withhold grain from state institutions. The controversy also highlighted a consultation problem: farmers’ representatives argued that the price had been set without sufficient participation by farmers’ unions or local producers, despite sharp regional cost differences.

This controversy is indicative of a broader problem in the local production-cost structure. Farmers argued that fertilizer, diesel, pesticides, harvesting, sacks, and transport costs had risen sharply, with some inputs effectively priced in dollars while the state purchase price was set in Syrian pounds. Farmers pointed to high costs for diesel, fertilizer, irrigation, harvesting, and transport, while others noted a discrepancy between the state’s wheat seed price of around USD 500 per ton and the initial crop purchase price of about USD 330 per ton. Farmers also explained that a single national procurement price also fails to reflect regional differences, especially in eastern governorates, where irrigation costs can be structurally higher than in rain-fed or better-served areas.

Protests Erupt over Closure of Makeshift Oil Refineries in Aleppo

Key Developments: The Syrian Petroleum Company’s (SPC) decision to close primitive oil refineries/burners, known locally as “harraqat”, in Tarhin near al-Bab in rural Aleppo, triggered protests by owners, workers, and traders in late May. Protesters argued that the facilities had operated for years under previous local arrangements, supplied fuel to northwestern Syria during the conflict, and supported thousands of direct and indirect livelihoods. Internal security forces prevented demonstrators from reaching Saadallah al-Jabiri Square in Aleppo on May 20, while other reports said tensions escalated in Tarhin as security forces moved to enforce the dismantling.

SPC and the Ministry of Energy defended the closures on legal, health, environmental, and technical grounds, saying the haraqaat were illegal, unsafe, highly polluting, and produced fuel that did not meet Syrian specifications. The SPC gave owners two options: sell the metal structures to the company at “incentive” prices or keep them, provided they signed a pledge not to use them again in any oil-related activity. The company also began interviews to place haraqaat workers at formal oil facilities and to settle outstanding financial dues owed to owners, while SPC later welcomed a pledge by Hemco Minerals and Fuels to remove its own primitive refineries in Aleppo.

Why It Matters: The makeshift oil refineries emerged because the formal fuel supply collapsed during the conflict, and in places such as Tarhin, they became a full local economy: supplying diesel to generators, bakeries, water pumps, agriculture, and transport, while providing work for displaced families with few alternatives. This is why the closure is socially sensitive. The government’s argument is rational: primitive refining is unsafe, polluting, technically inefficient, and outside formal fuel regulation. Still, the sector had been tolerated, taxed, organized, or indirectly managed by successive local authorities for years, creating expectations of recognition, compensation, or gradual transition.

Shutting down the haraqaat is part of a necessary post-war normalization of the oil sector: centralizing crude flows, ending low-quality refining, reducing waste, improving safety, and returning fuel processing to formal infrastructure. But if the state closes these facilities without a credible livelihood plan, the risk of social unrest is real, as seen in these early demonstrations.

Similar tensions to those in Aleppo appeared earlier in Deir Ezzor. In February 2026, Damascus ordered the closure of informal refineries, and workers protested almost immediately, arguing that the decision threatened surrounding livelihoods. While the SPC seems to be keen on absorbing workers into formal oil facilities, workers said the job offers lacked clarity on salaries, contracts, locations, and guarantees.

Damascus Offers Marota and Basilia Compensation Package, but Decree 66 Dispute Deepens

Key Developments: In May, Damascus Governorate took steps to address long-standing grievances related to Legislative Decree No. 66 of 2012, the framework governing Marota City and Basilia City. Officials presented the measures as an effort to correct past injustices while continuing the two projects, which cover parts of Mazzeh, Kafr Sousa, Daraya, Qadam, Nahr Aisha, and the southern ring-road area. The governorate said it had received 1,606 grievance requests, resolved 1,122, increased owners’ allocated floor area by 13.9%, raised rent allowances for alternative-housing beneficiaries by 35 times, restored rights to more than 1,000 previously excluded families, and allocated funding to build 54 alternative-housing towers over three years. It later began paying rent allowances to eligible beneficiaries in Marota City.

Yet, the package did not settle the dispute. Affected owners and rights advocates argued that Decree 66 had converted direct property ownership into shares inside a governorate-managed project, while the Association to Repeal Decree 66 and Restore Rights demanded cancellation of the decree and return of confiscated property. Affected groups say more than 12,000 homes were demolished in Marota-linked areas and more than 20,000 homes in Basilia-linked areas, with tens of thousands displaced.

The controversy also took on a political and rights dimension following the arrest of activists. Affected residents had organized repeated protests demanding the repeal of Decree 66, while Hashtag Syria reported that two representatives of affected owners, Ibrahim Sheikh al-Shabab and Yasser Abbas, were detained after Damascus Governor Maher Idlibi filed a complaint with the cybercrime branch regarding their media and protest activities. Critics said the compensation measures remain insufficient because the file concerns not only urban planning, but also property rights, forced displacement, investor accountability, and transitional justice.

Why It Matters: Grievances linked to Legislative Decree No. 66 of 2012 are long-standing and extend far beyond questions of compensation. For many affected residents, the issue concerns displacement, the loss of community ties, uncertainty surrounding alternative housing, and the conversion of direct property ownership into shares whose value and future remained unclear. Residents repeatedly argued that the project converted homes and land into regulatory shares of uncertain value, while years of delays, low rental allowances, and a lack of clarity about alternative housing forced many families to sell their rights at heavily discounted prices. Others argued that ownership requirements failed to account for families whose documents had been lost, destroyed, or left behind during years of displacement.

Following the collapse of the Assad regime, affected and advocacy groups saw an opportunity to reopen a file that had long been politically untouchable. Residents’ committees and activists have pushed not only for higher compensation, but also for greater transparency, recognition of past grievances, and, in some cases, revisions to the master plans themselves.

The new authorities are attempting to address some of the decree’s consequences without abandoning the framework altogether. While the compensation package is significant, it remains a corrective measure within the existing system rather than a full legal reset. Many affected owners argue that the problem is not only inadequate compensation, but the original conversion of property rights into shares in a governorate-managed project. For many residents, the issue is also one of return, with alternative housing elsewhere seen as an insufficient substitute for homes and communities lost in areas such as Mazzeh, Kafr Sousa, Qadam, and al-Assali.

At the same time, a full reversal would be difficult after more than a decade of accumulated contracts, shares, and property transactions. The broader debate over Jobar, Qaboun, and Tishreen suggests that Marota could set a precedent for reconstruction across Syria. How the government handles this file may ultimately determine whether reconstruction strengthens confidence in property rights or becomes an early legitimacy crisis of the transition.

About the Syria Monthly Economic Digest

The Syria Monthly Economic Digest is a monthly publication by The Syria Dispatch that tracks the political and economic developments shaping Syria’s transition.

Each edition selects the developments I consider most significant over the past month; not every headline, but the ones that reveal something important about where the country is heading. These may include policy decisions, investment announcements, energy and infrastructure developments, banking and monetary reforms, trade and reconstruction dynamics, property rights disputes, public service issues, and the evolving relationship among the Syrian state, society, and external actors.

The format is simple: each entry begins with a news summary explaining what happened, followed by a “Why It Matters” section offering additional information, context, and analysis.

The digest is written for readers who want a structured, analytical overview of Syria’s transition: policymakers, researchers, journalists, diplomats, development practitioners, investors, civil society actors, and anyone trying to follow the country’s economic and political trajectory.

It is not intended to be exhaustive, and it does not replace daily news monitoring. Instead, it offers a monthly snapshot of the issues I believe deserve closer attention.

For comments, corrections, suggestions, or collaboration inquiries, please feel free to reach out.

I just discovered this and it is fantastic